At its heart, small business bookkeeping is about one simple thing: knowing where your money is going. It’s the habit of keeping a careful record of every dollar that comes in and every dollar that goes out. Think of it as the financial pulse of your company—the one thing that tells you if you're healthy, growing, or headed for trouble.

Why Bookkeeping Is Your Business Superpower

Let's be honest, for most entrepreneurs, the word "bookkeeping" sounds like a chore. It brings to mind tedious spreadsheets and confusing jargon, and it's often the first thing to get pushed to the bottom of the to-do list.

But I want you to reframe that. Bookkeeping isn't just about compliance or taxes; it’s about control. It's the dashboard for your entire business.

Imagine trying to drive a car with the windows blacked out and no gauges. You wouldn’t know how fast you were going, how much fuel you had left, or if the engine was about to overheat. Running a business without solid bookkeeping is exactly like that—you're flying blind, making guesses, and hoping for the best.

From Financial Chaos to Strategic Control

When your finances are a jumbled mess, it’s impossible to make smart decisions. This is a huge reason so many new businesses stumble. In fact, a study found that roughly 60% of small business owners don't feel confident about their accounting knowledge, and a shocking 82% of business failures are tied directly to poor cash flow management. You can explore more data on how bookkeeping impacts business success.

Getting a handle on your books changes everything. It helps you:

- Make Confident Decisions: Suddenly, you know exactly how much cash is in the bank, who owes you money, and which bills are coming due. This clarity gives you the confidence to know when it’s the right time to hire a new employee, invest in equipment, or launch that big marketing campaign.

- Boost Your Bottom Line: When you categorize your expenses properly, you can see exactly where every dollar is going. Are you overspending on software subscriptions? Is one marketing channel outperforming all the others? This is how you find opportunities to cut costs and double down on what works.

- Stay Tax Ready, Always: Clean books turn tax time from a frantic nightmare into a calm, predictable event. You can easily pull the reports your accountant needs, maximize every possible deduction, and avoid the stress and penalties that come with last-minute filings.

Bookkeeping isn't just about recording what happened in the past. It’s about lighting up the present so you can build a more profitable future. It turns raw financial data from a source of anxiety into your most valuable strategic tool.

Ultimately, good bookkeeping is your early warning system, your roadmap to growth, and your proof of performance, all rolled into one. It’s the foundational discipline that separates the businesses that thrive from the ones that don't make it.

Building Your Financial Foundation

Before we dive into the day-to-day tasks, we need to get a handle on a few core ideas. Think of these as the foundation of your financial house—get them right, and everything else you build on top will be solid and stable. These aren't complicated theories, just practical concepts that bring order to your business's finances.

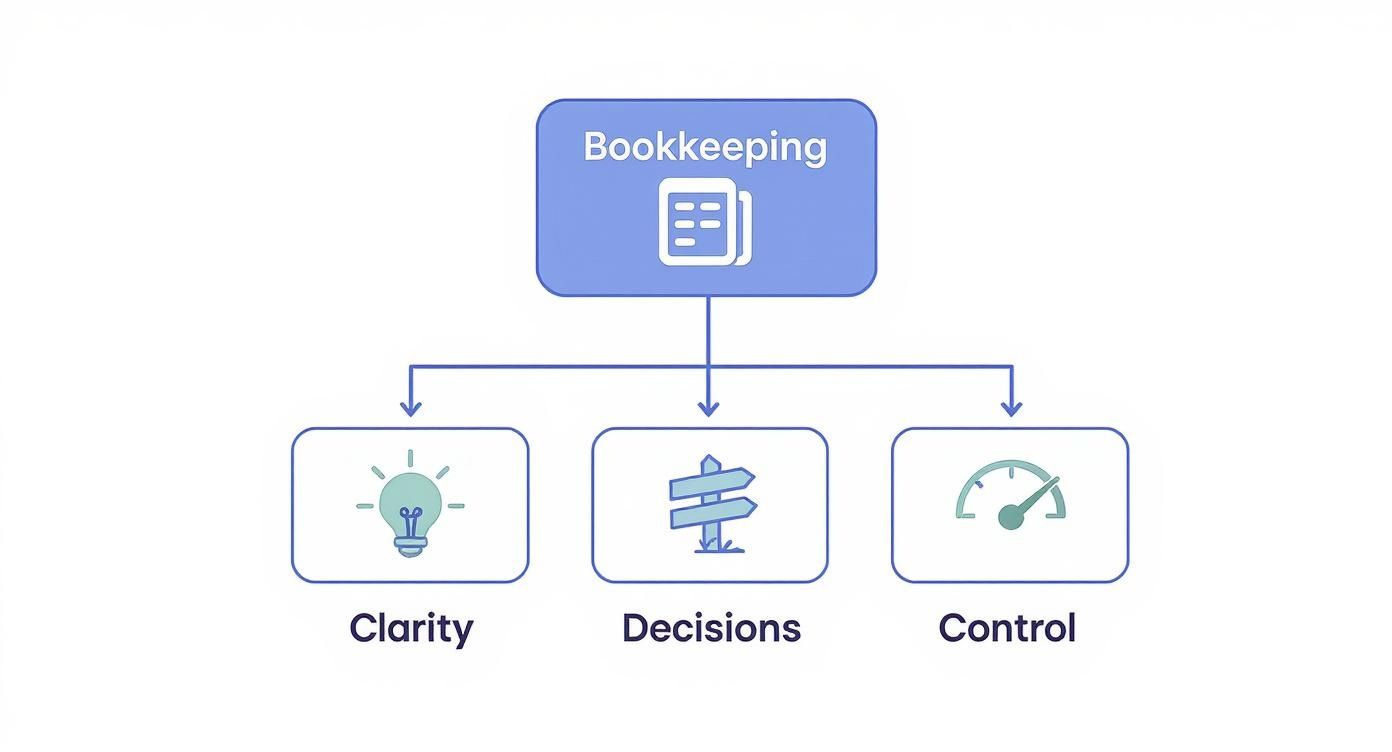

First up is the Chart of Accounts. This is the single most important organizational tool you have. Imagine it as a detailed filing cabinet for your money. Every single dollar that comes in or goes out has a specific folder. A payment from a client? That goes into a "Sales Revenue" folder. The monthly fee for your project management software? That gets filed under "Software Expenses." This simple act of categorization is what lets you see exactly where your money is coming from and where it's going.

This simple structure is what unlocks the true power of good bookkeeping.

As you can see, organizing your records brings clarity. That clarity lets you make smarter decisions, which ultimately gives you real control over your business's future.

The Accounting Equation Made Simple

Now, let's look at how those "folders" in your Chart of Accounts are grouped. Every transaction fits into one of three main categories that work together in a simple, unshakable formula. Don't let the word "equation" scare you; it's basic math.

- Assets: This is all the valuable stuff your business owns. It’s the cash in your bank account, the laptop you work on, office furniture, and even the money that clients still owe you (that’s called accounts receivable).

- Liabilities: This is everything your business owes to other people. Think of business loans, credit card balances, or bills from your suppliers that you haven't paid yet (known as accounts payable).

- Equity: This is what’s left for you, the owner, after you subtract what you owe (liabilities) from what you own (assets). It’s the net worth of your business.

The big secret? They always have to balance out like this: Assets = Liabilities + Equity. This is the golden rule of bookkeeping. Every transaction you record has to keep this equation in balance, which is how you know your books are accurate.

Choosing Your Bookkeeping Method

Finally, you need to decide how you'll record all these transactions. There are two main approaches, and the difference really comes down to timing.

Single-entry bookkeeping is the most straightforward method, working a lot like your personal checkbook register. You simply log money when it comes in and when it goes out. It's easy to learn but doesn't give you the full picture and can make it easy for errors to slip through unnoticed.

Double-entry bookkeeping, however, is the standard for any serious business. For every transaction, it makes two entries—a debit in one account and a credit in another. It's like a perfectly balanced scale: for every action, there is an equal and opposite reaction. This system is incredibly powerful for catching mistakes and is an absolute must-have if you plan on growing your business.

Setting Up Your Bookkeeping System

Now that you've got the basic concepts down, it's time to roll up your sleeves and build the system that will keep your finances in order. A solid setup is the bridge between knowing what to do and actually doing it consistently. The first big choice you'll make is what tool you'll use to track every dollar that comes in and goes out.

Many new business owners instinctively reach for a spreadsheet. It feels simple, it's cheap (or free), and it's familiar. But that comfort can quickly turn into a headache. Spreadsheets are notorious for manual errors, they become incredibly clumsy as your business grows, and they lack the automation that modern tools offer.

This is why a whopping 64.4% of small business owners have already made the switch to accounting software. Platforms like QuickBooks Online or Xero aren't just a trend; they're the new standard for a reason. They automate the grunt work and give you back precious hours.

Before you decide, let's break down the real-world differences between sticking with a spreadsheet and investing in dedicated software.

Choosing Your Bookkeeping Tool: Spreadsheet vs. Software

| Feature | Spreadsheet (e.g., Excel, Google Sheets) | Accounting Software (e.g., QuickBooks, Xero) |

|---|---|---|

| Cost | Free or low one-time cost. | Monthly subscription fee (typically $20-$70). |

| Automation | None. All data entry is manual. | Automatically imports bank transactions, saving hours. |

| Accuracy | High risk of typos, formula errors, and accidental deletions. | Minimizes human error with built-in checks and automation. |

| Reporting | Manual creation of financial reports, which is time-consuming. | Generates professional reports (P&L, Balance Sheet) with one click. |

| Collaboration | Difficult to share securely with an accountant or team. | Easy, secure access for your bookkeeper, accountant, and team. |

| Scalability | Becomes unwieldy and slow as transaction volume increases. | Easily scales with your business from one to thousands of transactions. |

| Integration | No direct connections to other business tools. | Integrates with payroll, payment processors (Stripe, Square), and more. |

For a brand-new side hustle with just a few transactions a month, a spreadsheet might work for a little while. But for any serious business, accounting software quickly pays for itself in time saved and mistakes avoided.

Building Your Chart of Accounts

Once you've picked your tool, the next step is setting up your Chart of Accounts. Remember that financial filing cabinet analogy? This is where you label the drawers. You're creating the specific categories (or "accounts") where every single transaction will live.

When you're starting out, keep it simple. You can always add more detail later. A basic Chart of Accounts for a service business might look something like this:

- Income: Sales Revenue, Service Fees

- Cost of Goods Sold (COGS): Materials, Subcontractor Labor

- Expenses: Advertising, Office Supplies, Software Subscriptions, Rent, Utilities

This framework is the absolute backbone of your bookkeeping. It’s what ensures every transaction is sorted correctly, which is the key to getting accurate reports and making tax time infinitely less painful. A well-organized system can save you a ton of stress, as we cover in our guide to cloud bookkeeping hacks for Washington businesses.

The Golden Rule of Setup: Keep your business and personal finances 100% separate. Open a dedicated business bank account and get a business credit card from day one. Mixing funds is the fastest way to create a tangled mess that will cost you a fortune in time and professional fees to fix.

Connect Your Bank Accounts

This last step is the real game-changer. If you take away only one thing from this section, make it this: connect your business bank and credit card accounts directly to your accounting software.

Doing this automates the single most boring part of bookkeeping. Instead of typing in every coffee shop meeting, supply order, and client payment by hand, the transactions flow into your software automatically every day.

Your job instantly transforms from tedious data entry to simple review. All you have to do is check in regularly and assign each transaction to its proper category in your Chart of Accounts. It’s a simple habit that keeps your books accurate and up-to-date with almost no effort, giving you a real-time pulse on the financial health of your business.

Your Daily, Weekly, and Monthly Bookkeeping Routine

Good bookkeeping isn't about one massive, heroic effort at the end of the year. It’s about building a simple, sustainable rhythm. Think of it less like a sprint and more like a daily walk. By breaking down the work into small, consistent chunks, you turn a mountain of a task into a manageable habit.

This approach keeps your financial records pristine and, more importantly, prevents that dreaded end-of-month (or end-of-quarter) scramble. It’s the key to truly understanding your business's financial health in real-time, allowing you to make sharp, informed decisions when it matters most.

https://www.youtube.com/embed/ewI_X5M_Awg

Your Daily Tasks: The Five-Minute Check-In

The goal for your daily tasks is simple: capture financial information while it's still fresh in your mind. This whole process shouldn't take more than five minutes, but it will save you hours of detective work later.

- Review and Categorize Transactions: If you’ve linked your bank accounts to your accounting software (and you definitely should!), new transactions will pop up daily. Just take a quick look and assign each one to the right category from your Chart of Accounts. Was that Amazon purchase for office supplies or personal stuff? Categorize it now.

- File Receipts Digitally: The moment you get a physical receipt for a business purchase, snap a photo of it. Most modern accounting platforms like QuickBooks Online or Xero have fantastic mobile apps that let you upload the image and attach it directly to the transaction it belongs to.

This tiny habit means every single expense is documented and ready for tax season. No more shoeboxes full of faded receipts!

Your Weekly Tasks: Staying Ahead of the Curve

Set aside a dedicated block of time—maybe 30 to 60 minutes every Friday afternoon—to manage your cash flow and keep the wheels turning. This is where you shift from just recording what happened to actively managing what’s happening next.

- Pay Your Bills: Take a look at your outstanding vendor invoices (your accounts payable) and schedule payments. This keeps you in good standing with your suppliers and helps you avoid frustrating late fees.

- Send and Follow Up on Invoices: Did you finish a project this week? Get that invoice out the door! While you're at it, check your accounts receivable report to see who hasn't paid you yet. A friendly, polite reminder can work wonders.

- Run Your Payroll: If you have employees, your scheduled payroll day is sacred. Process it consistently to make sure your team is paid accurately and on time, every time.

A consistent weekly routine is your best defense against cash flow problems. It keeps money coming in and going out predictably, which is the absolute lifeblood of any small business.

Your Monthly Tasks: The Big-Picture Review

Once a month, it's time to zoom out. Block off a few hours to formally "close" your books and analyze how your business actually performed. This is your chance to stop working in the business and start working on it.

- Reconcile Your Bank Accounts: This is the most important task on the list. You must do it. Go through your bank and credit card statements line by line and match them against the transactions in your bookkeeping software. This process is the only way to confirm your books are 100% accurate.

- Review Financial Statements: Now for the fun part! Generate your key reports—the Profit & Loss Statement and the Balance Sheet. What do they tell you? Look for trends. Are your sales growing? Did a certain expense category spike unexpectedly? This is where you get the insights to steer the ship.

- Prepare and File Tax Returns: Many small businesses have recurring tax obligations. If you operate in Washington, for example, you likely have monthly or quarterly B&O taxes to file. The end of the month is the perfect time to calculate what you owe and get it submitted.

How to Understand Your Financial Reports

Your bookkeeping system is constantly humming along in the background, grabbing and sorting data with every single transaction. But all that hard work is only helpful if you can actually understand the story the numbers are trying to tell. That’s where your financial reports come in—they translate all that raw data into real-world business intelligence. And don't worry, you absolutely do not need an accounting degree to figure them out.

For most small business owners, getting a handle on your books means really getting to know two key reports. They each give you a completely different, yet equally critical, view of your company’s health. I like to think of them as your business’s report card and a financial snapshot.

The Profit and Loss Statement: Your Business Report Card

The Profit and Loss (P&L) Statement, which you'll also hear called an Income Statement, is exactly what it sounds like: a report card for a specific chunk of time. It could be for a month, a quarter, or the whole year. Its job is to tell you one simple, crucial thing: did you make money or lose money?

The formula is pretty straightforward:

- Revenue (Income): This is your top line. It’s all the money your business brought in from selling your products or services during that period.

- Cost of Goods Sold (COGS): These are the costs directly tied to what you sell. If you run a coffee shop, this is your coffee beans and milk. If you're a consultant, it might be what you paid a subcontractor who helped on a project.

- Expenses: This bucket holds all the other costs of doing business—the money you spent just to keep the lights on. Think rent, software subscriptions, marketing, and payroll.

Subtract your COGS and your other expenses from your revenue, and you get your Net Income. This is famously known as the "bottom line." If it's a positive number, congratulations, you turned a profit. If it’s negative, you took a loss for that period.

The P&L is all about performance over time. It answers the question, "How did we do last month?" This is your go-to report for spotting trends, like creeping expenses or seasonal sales dips, giving you the chance to make strategic adjustments.

The Balance Sheet: A Financial Snapshot

While the P&L statement shows you how you did over a stretch of time, the Balance Sheet gives you a snapshot of your business's financial health on one specific day. It lays out exactly what your company owns, what it owes, and what's left for you, the owner.

It’s built on that fundamental accounting equation we talked about earlier: Assets = Liabilities + Equity.

- Assets: This is all the valuable stuff your business owns. It includes everything from the cash in your bank account and the computers on your desks to the money your clients still owe you (that’s Accounts Receivable).

- Liabilities: This is everything your business owes to others. It’s your credit card balances, outstanding vendor bills, and any business loans you might have.

- Equity: This is the value that’s left after you subtract all the liabilities from the assets. It essentially represents the owner’s stake in the company.

There’s a reason it’s called a Balance Sheet—it literally has to balance. The two sides of that equation must always be equal. This report is the ultimate measure of your company’s stability and is exactly what a bank will want to see if you ever apply for a loan.

When you look at them together, the P&L and the Balance Sheet give you a truly complete picture of your financial reality.

When Should You Outsource Your Bookkeeping?

Handling your own books in the early days is a fantastic way to get your hands dirty and truly understand the financial pulse of your business. It gives you a sense of control that’s invaluable. But as your business starts to take off, that same hands-on approach can start to hold you back.

The question isn't if you'll outgrow DIY bookkeeping, but when. The decision to hand over the reins isn't about admitting defeat; it’s about making a smart, strategic play to get your most precious resource back: your time. If you’re spending more late nights tangled in spreadsheets than you are talking to customers or dreaming up your next big move, that’s a red flag. Your time is being spent in the business, not on it.

The Telltale Signs It's Time for a Pro

Think of it like this: you wouldn't keep fixing a leaky pipe yourself once your house has a second story and complex plumbing. The same goes for your finances. There are a few classic signs that you're ready to bring in a professional. Spotting them early can save you a world of headache and money.

You should seriously start looking for help if you're nodding along to any of these:

- Things Are Getting Complicated: You've added payroll, started tracking inventory, or now have to navigate the wonderful world of sales tax. The simple in-and-out of a year ago is long gone.

- It's a Time Sink: You’re consistently spending more than 5-10 hours every single month just trying to keep the books in order.

- Mistakes Are Costing You: You’ve found errors that led to tax penalties, overdraft fees, or—worse—you’ve made a big decision based on numbers that turned out to be wrong.

- You're Flying Blind: You look at your financial reports and feel more confused than confident. You aren't sure what the numbers are actually telling you about the health of your business.

Outsourcing bookkeeping isn’t just another expense on the list. It’s an investment in getting it right, saving time, and buying back your sanity. It frees you up to do the things only you can do to grow the business.

Making this leap is more common than you might realize. A whopping 78% of small businesses around the world now outsource their bookkeeping, a clear signal of its value. To meet that need, there are over 335,000 bookkeeping and payroll firms in the U.S. alone. You can read more about the rise of outsourced bookkeeping on amraandelma.com.

When you feel you’re ready to see what professional help looks like, a great first step is learning about the different bookkeeping services available to find the right fit for your business.

Answering Your Top Bookkeeping Questions

Once you start getting into the weeds of your business finances, a few specific questions always seem to come up. Let's walk through some of the most common ones I hear from small business owners.

What’s the Real Difference Between Bookkeeping and Accounting?

It’s a great question, and it's helpful to think of it like building a house.

Bookkeeping is the day-to-day construction work. It's the essential job of laying the foundation and framing the walls by recording every single financial transaction—every sale, every expense, every payroll run. It's all about creating a solid, accurate structure.

Accounting, on the other hand, is the architect's role. An accountant takes the structure the bookkeeper built, analyzes it, creates the blueprints (your financial statements), and helps you strategize. They help you see the big picture and plan for the future. You can't have one without the other; bookkeeping creates the data, and accounting turns that data into valuable insight.

How on Earth Do I Handle Crypto Transactions?

Ah, crypto. It definitely adds a wrinkle to your books, but it's manageable once you understand the rules. The IRS sees cryptocurrency as property, not currency. This is a crucial distinction. It means almost every move you make—buying, selling, or even trading Bitcoin for Ethereum—is a taxable event.

The name of the game is meticulous tracking. For every single transaction, you absolutely must record the date, the fair market value in U.S. dollars at that exact moment, and what the transaction was for. This is the only way you’ll be able to accurately calculate your capital gains or losses when tax time rolls around.

This gets complicated in a hurry. I strongly recommend using software built specifically for this. You can find a breakdown of some of the best bookkeeping and crypto tax tools to keep things simple and, more importantly, compliant.

Can I Really Do My Own Bookkeeping?

Yes, you absolutely can, especially when you're just starting out. Modern software has made the basics of bookkeeping more user-friendly than ever, and doing it yourself is a fantastic way to get an intimate understanding of your company's cash flow.

But the real question isn't can you do it, but should you? Think about the value of your time. If you're spending hours each week wrestling with receipts and reports—time you could be using to land a new client or improve your product—then outsourcing might actually be the more profitable move. It's a simple cost-benefit analysis: weigh the cost of a pro against the revenue you could be generating with those hours back in your day.

Ready to trade financial stress for strategic clarity? The experts at Bugaboo Bookkeeping can handle the details so you can focus on growth. Schedule your free consultation today!

Article created using Outrank